West Africa’s Textile & Apparel market is rapidly expanding. Although considered nascent when compared to Asia’s more developed markets, it’s many greenfield opportunities also mean there are fewer legacy challenges to contend with. This offers a ripe opportunity for investors and manufacturers to start from an almost clean slate, which is crucial as the apparel industry makes strides toward a more environmentally sustainable footprint.

The region also has numerous natural and competitive advantages for textiles and apparel manufacturing and has seen increased interest from global actors, brands, manufacturers, infrastructure developers, development finance institutions, etc., over the last few years.

Impact of COVID

Most existing garment manufacturers pivoted to producing PPE for both domestic and international markets. For instance, DTRT is making this a permanent feature of their production, although orders have resumed from their traditional apparel buyers.

We have also witnessed a stronger resolve from governments to support their domestic T&A manufacturing sectors’ growth. The Togo deal, for instance, happened at the height of covid lockdowns. Some countries also offered waivers on value-add tax for their textile and apparel manufacturers and used the time to restructure their labor codes to meet international standards.

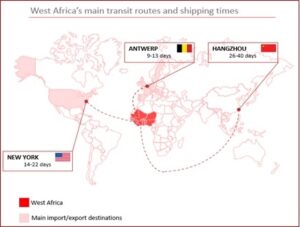

Understanding West African countries’ competitiveness as an apparel-sourcing base for western fashion companies

First, there is an immense opportunity to vertically integrate the T&A manufacturing value chain. The region produces around 1.5 million metric tons of cotton annually, which represents about 60% of Africa’s total output and 15% of global exports. The vast majority of this is exported unprocessed. Farming methods feature rain-fed irrigation with harvest done by handpicking, leading to 80% being labeled as preferred, sustainable cotton under Better Cotton Initiative (BCI) and Cotton made in Africa (CmiA) standards.

Secondly, its geographical location means it offers a natural nearshore market to Europe and US markets – literally less than two weeks away from Europe by sea.

Other benefits include an abundant trainable labor force, cost savings to manufacturers under favorable trade instruments like African Growth and Opportunity Act (AGOA), EU’s Economic Partnership Agreement (EPA)/Everything But Arms (EBA) program, etc., as well as consolidated political stability in all three countries. Moreover, there is strong potential for developing a circular textile economy facilitated by green manufacturing and initiatives.

Apart from the main retail regions, there is a growing online retail market in Africa – estimated to increase to $75 billion by 2025 with projected $3.4 trillion aggregate GDP under African Continental Free Trade Area (AfCFTA). As we have seen with recent moves to the continent by Twitter, Google, and others, there is large scope for fashion retailers to use manufacturing in West Africa as a launchpad into this growing continental market, with free movement of goods and services under AfCFTA.

These are attractive propositions for buyers and manufacturers looking to diversify their supply chains and leave a greener carbon footprint in the process.